Non-EU Companies at Paris 2024 Olympics: Get your VAT back!

Tax alertCompanies Paris 2024 VAT

By: Stéphany Brévost, Thibaut Grange, Philippine Schlemer

15 Jan 2024 6 min read

On 30 December 2023, the Finance Act for 2024 (“LDF24”) was published, following its approval by the French Constitutional Council on 28 December 2023. The Act includes significant measures relating to corporate tax.

Transposition of the « Pillar 2 » directive (Art. 33)

One of the key measures presented in the PLF24 is the transposition of the EU directive aimed at ensuring a minimum level of international taxation for groups of companies in accordance with the Global Anti-Base Erosion (GloBE) rules.

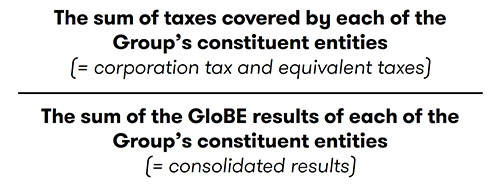

This measure introduces a minimum tax rate of 15% on the profits of multinational and national groups of companies with an annual consolidated turnover of €750m or more in at least 2 of the 4 financial years preceding the financial year in question.

The effective tax rate (ETR) of the Group will have to be determined for each State or territory and for each financial year in accordance with the following formula:

In the event of a tax shortfall in a jurisdiction, the additional corporate tax can be collected through 3 different mechanisms:

The annual minimum tax applies to fiscal years beginning on or after 31 December 2023 (except for the RBII part which will only come into force for tax years beginning on or after 31/12/2024).

The LDF24 also includes a provision for temporary tax relief for financial years beginning before 31 December 2026 and ending no later than 30 June 2028, based on the CbCR declaration whereby the additional tax is deemed to be nil in a jurisdiction if:

Introduction of a tax credit for investments in green industry (Art. 35)

The LDF24 provides for the creation of a tax credit for investments in green industry (C3IV), to be granted to companies which invest in capital expenditure other than for capital replacement, and in activities which contribute to the production of batteries, solar panels, wind turbines or heat pumps.

The rate of the C3IV is 20% and increased to 25% or 40% according to the geographical zone of the investment. The total amount of the C3IV is capped at €150m per company (raised to €200m or €350m in regionally aided zones “ZAFR” or outermost regions “RUP”).

The C3IV is granted with prior approval, and subject to the investments being carried out in compliance with tax, social and environmental legislation over a minimum of 5 years (3 years for SMEs), to companies that can demonstrate the following:

The C3IV will apply to approved investment projects until 31 December 2025

Changes to the measure for innovative young companies “JEI” (Art. 44 et 48)

As from 1 January 2024, the LDF24 cancels the corporate tax exemption for the creation of innovative young companies or “JEI”, considering this measure to be no longer necessary (the exemption from social security contributions is, however, maintained).

The status of JEI is extended by the creation of a new category of company: JEC or « jeunes entreprises de croissance » (young high-growth companies), corresponding to SMEs where between 5% and 15% of total expenditure is in R&D and where certain economic performance indicators defined by decree are met.

Dividends and the share of costs and expenses “QPFC”: brought into line with case law (Art. 52)

In accordance with European case law (ruling of 11 May 2023 of the Court of Justice of the European Union relating to the companies Manitou BF and Bricolage Investissement France), the reduced rate of 1% for the share of costs and expenses (QPFC) and the 99% exemption (where a company’s dividends do not qualify for the parent-subsidiary regime) will now apply to all dividends received from European subsidiaries that meet the conditions for forming an integrated group with their French parent company, and this regardless of whether or not the latter has opted for tax consolidation.

However, dividends paid between companies established in France that have voluntarily opted not to form an integrated group despite meeting the conditions for doing so, remain subject to tax.

Lastly, the LDF24 re-introduces a minimum period of belonging to a tax group of one financial year before qualifying for the reduced rate of 1%, during which the dividends distributed between member companies will be subject to the rate of 5% of the QPFC.

These measures apply to financial years ending as from 31 December 2023.

Postponement of the abolition of the CVAE (Art. 79)

The abolition of the CVAE will be staggered until 2027 with a gradual reduction in the maximum tax rates (i.e. 0.28% for 2024, 0.19% for 2025, 0.09% for 2026).

Concerning the minimum contribution on the value added of companies (€63), this will be abolished from 2024.

Deferral of electronic invoicing obligations (Art. 91)

The initial dates set for the obligation of companies to e-invoice and for certain e-reporting obligations to the French authorities have been deferred:

Implementation of the anti-fraud plan (Art. 112 et 113)

The LDF24 implements a number of measures relative to the repressive tax matters of the plan in order to combat all forms of public finance fraud, such as:

Greater flexibility of the conditions for carrying out controls (Art. 117)

Audits of a company’s accounts and on-site inspections may now in exceptional cases be carried out away from the company premises, provided that the taxpayer consents.

Tax officials will also be able to carry out their duties anonymously.

These measures will apply as from 1 January 2024 and to tax audits already in progress and undertaken on or after that date.

Transfer Pricing (Art. 116)

Find out more about the measures relating to transfer pricing in the special alert written by our experts here.

Following the publication of the Finance Act for 2024 on 30 December, we outline below some of the more significant measures of interest to individual taxpayers in France.

Finance Act 2024 Transfer pricing