As of January 1, 2022, French VAT-registered entities must reverse-charge (and simultaneously recover) French import VAT on French VAT returns filed before the French Tax Administration rather than, as in the past:

- Either having to pay French import to the French Customs Authorities and then only be able to recover it on French VAT returns later (i.e., negative cash impacts),

- Or applying for an authorization from the French Customs Authorities enabling reverse-charging French import VAT and simultaneously recovering it directly on French VAT-returns.

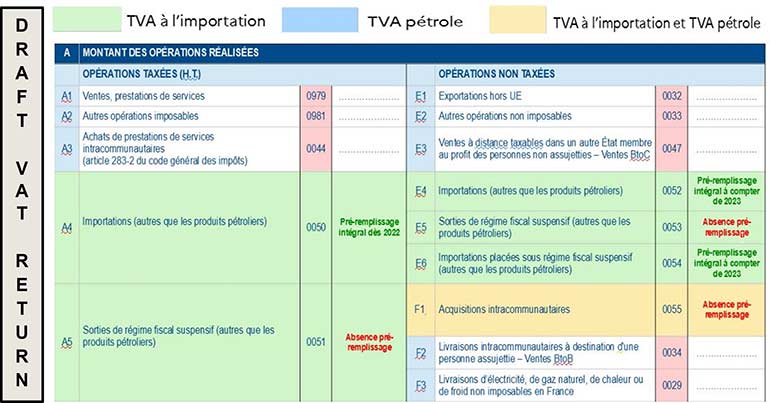

In preparation, the French Tax Administration has updated the French VAT return form, which will get a facelift.

The draft new VAT return, reproduced below, will permit the effective reverse-charge of French import VAT by all French VAT-registered companies, irrespective of whether they are established in France.

In practice, the net amount and corresponding import VAT from the French import declaration will be automatically electronically transmitted to the French Tax Authorities to pre-fill the French VAT returns.

France now joins other European countries (such as Sweden, Belgium, Italy, Ireland, Poland, Netherlands, Germany) having implemented an automatic mandatory import VAT reverse-charge mechanism.

The overhaul of the French VAT return form, including certain pre-filled boxes and mandatory import VAT reverse-charge, is an overdue revolution for which we can assist with any questions on how to declare and recover French VAT.

Authors

-

Amanda Quenette

Avocate Manager -

Tommy Meziane Petersen

Attorney-at-law