Reform of the French General Accounting Plan

Tax alertThe entry into force of the 2025 General Accounting Plan (PCG), resulting from ANC Regulation 2022-06, marks a significant development for businesses.

By: Romain Dayan, Robin Maubert, Pascal Luquet, Mickaël Duquenne

29 May 2026 3 min read

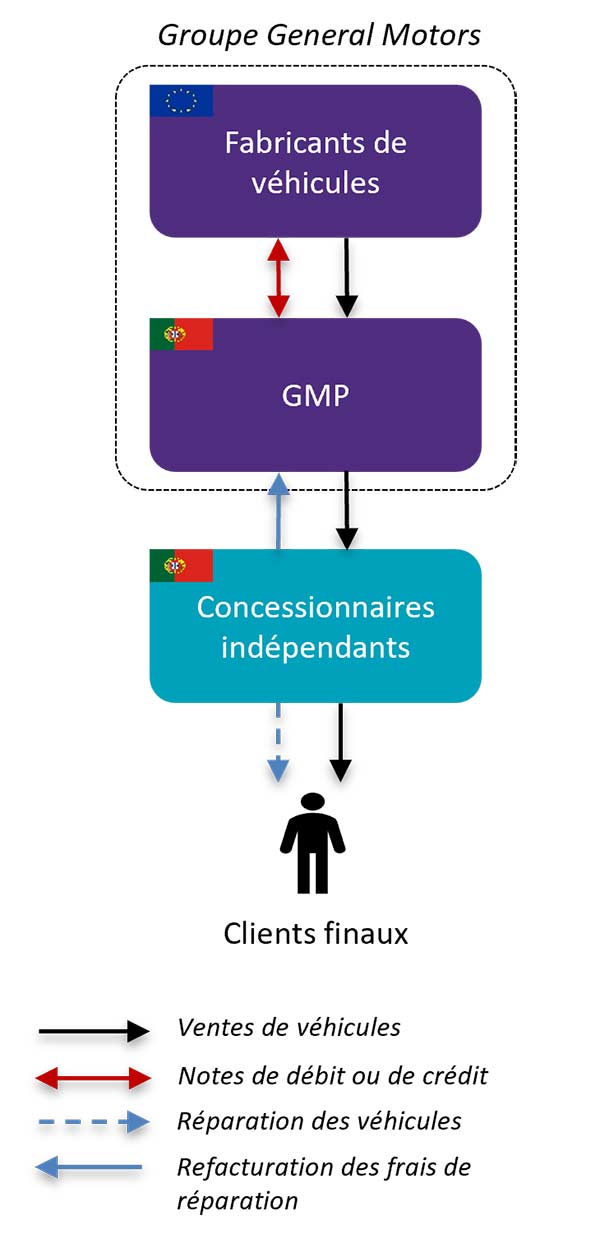

In a decision of 13 May 2026 (Stellantis Portugal, C-603/24), the CJEU ruled again on the connection between transfer pricing adjustments and VAT.

The facts: Stellantis Portugal (ex General Motors Portugal) purchased vehicles from affiliated car manufacturers and resold them to independent dealers, while managing after-sales activities, notably including reimbursing dealers for costs related to warranty repairs.

In accordance with the Group’s TP policy, year-end adjustments were made to the initial selling prices of the vehicles (through credit or debit notes) so GMP would achieve a pre-agreed operating-profit margin. The calculation of the adjustments considered, among other factors, the costs associated with vehicle repairs.

The Portuguese Tax Authorities considered that these adjustments constituted consideration for a VAT-taxable separate supply of repair services provided by GMP to the manufacturers.

Relevance of the Case: this decision forms part of the continuing debate on the VAT treatment of TP adjustments, and more broadly the interaction between VAT and TP. In the absence of harmonized guidance at EU level, this issue had previously been largely left to litigation and the interpretation of national courts.

The entry into force of the 2025 General Accounting Plan (PCG), resulting from ANC Regulation 2022-06, marks a significant development for businesses.

The French Finance Act for 2026 allows the use of a market rate for the deductibility of interests paid to minority corporate shareholders for fiscal years ending on or after December 31, 2025. To date, being an associated company was the only way to exceed the reference rate.

La Loi de finances est arrivée, et notre webinaire Arrêté des Comptes 2025, organisé le jeudi 19 mars 2026, est désormais disponible en replay