Impatriate tax regime

Tax AlertImpartiate Tax Regime, determination applicable remuneration professional soccer player

By: Anne Frede, Edouard De Raismes, Clervie Corvoisier, Lamia Mahrouk

22 Apr 2026 11 min read

The Finance Act for 2026 (FA 2026) was adopted in its final reading by the French National Assembly on 2 February 2026. With the Constitutional Council approving most of its provisions, the Act was published in the Official Journal on 20 February 2026.

Several measures that were initially proposed were finally dismissed, notably the imposition of a tax on high-net worth individuals, the cancellation of tax relief on pensions and retirement benefits, the reform of the capital gains tax regime on property, and the reform of retirement savings plans. The Dutreil Pact was the subject of heated discussions and was repeatedly challenged throughout the parliamentary debates. The amendments adopted, which modify its regime, are themselves the result of compromise solutions.

This article provides an overview of the main provisions of the 2026 Finance Act relating to personal taxation.

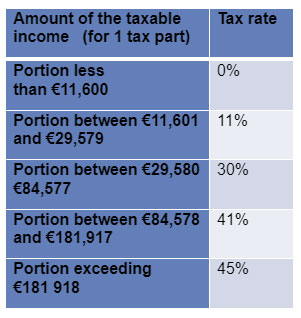

The CDHR applies to income earned in 2025, so as to ensure a minimum tax rate of 20% for the wealthiest taxpayers who are French tax residents and whose taxable income following tax adjustments:

The contribution is equal to the positive difference between; on the one hand, the contribution resulting from applying a 20% rate to the tax household’s income and any reduction; and, on the other hand, the sum of the income tax and the exceptional high-income contribution after adjustments.

In practice, this contribution has mainly affected taxpayers receiving investment income and capital gains subject to the 12.8% flat-rate levy.

Initially planned for one year, this tax contribution has been extended indefinitely and will remain in place until such time as the general budget deficit falls below 3% of GDP.

Several technical adjustments relating to the calculation of this contribution have also been made. These adjustments will have an impact on:

All of these changes will apply from the 2026 tax year onwards.

The income tax brackets have now been adjusted and indexed to the inflation rate (+0.9%).

The withholding tax rates have also been updated as of 1 May.

The Dutreil tax measure allows 75% of the value of the company's securities to be exempt from transfer taxes (donation or inheritance).

This exemption initially applied to businesses carrying out an eligible activity, where the shares are subject to a collective commitment to hold the shares for a period of two years, followed by an individual conservation commitment by the donee or heir to hold the shares four years.

Seven types of assets are now excluded from the 75% exemption where they are not used exclusively for the company's business activities. These include in particular:

These exclusions apply whether the asset is held by the company whose shares are being transferred or by its controlled subsidiaries.

To qualify for the 75% exemption, such assets must have been used exclusively for the purposes in question for a minimum period of three years prior to the transfer or, failing that, from the date of acquisition until the end of the individual commitment to retain them, or until their disposal. This condition is assessed at the level of the company holding the assets.

The duration of the individual holding commitment has now been extended from 4 to 6 years.

The “assumed agreement” arrangement, characterised in particular by the donee holding a management position following the transfer is in fact retained.

Similarly, the anti-abuse clause initially proposed to regulate any transfers carried out via family buy-outs (FBOs) has not been retained.

These new provisions apply to transfers taking place on or after 20 February 2026, with some uncertainty surrounding the extension of the individual conservation commitment period to those provisions already underway.

Contribution-transfer: amendment to the conditions for maintaining tax deferral (Article 11)

Capital gains arising from the contribution of securities to a company controlled by the contributor are automatically subject to a tax deferral.

Until now, in the event of the sale of the contributed securities within three years, the deferral was conditional upon the reinvestment of 60% of the proceeds from the sale in eligible assets in the company within two years.

The assets acquired had to be held for a period of one year from the date of their inclusion in the company’s assets, or for a period of 10 years in the case of indirect reinvestment (such as private equity structures).

The 2026 Finance Act introduces a number of significant changes.

The proportion of capital gains that must now be reinvested in order to qualify for the tax deferral has been increased to 70%. This is offset by an extension of the period allowed for reinvestment of the proceeds from the sale to three years.

The definition of eligible activities has been narrowed down.

Activities of a financial or property nature, as well as those generating guaranteed income due to the existence of a fixed tariff, are now expressly excluded from the scope of eligible reinvestments.

This exclusion essentially covers all property-related activities in the broadest meaning of the term: property development, land subdivision and property trading, as well as the activities of estate agents and property managers. The acquisition of hotel businesses, however, should not be impacted.

Furthermore, the holding period for assets or securities acquired as part of the reinvestment has been extended to five years.

In the event of a gift of securities for which capital gains tax is deferred, the deferral is transferred to the donee, provided the latter controls the company whose securities are being transferred. The donee is liable for tax on the deferred capital gains in the event of a disposal, contribution, redemption or cancellation of the securities occurring within five years of the gift. This period is now extended to 6 years from the date of acquisition. Similarly, this period is extended to 11 years (instead of 10 years) in the event of indirect reinvestment.

These new provisions apply from 20 February 2026.

Management Packages (Article 24)

For further details on the changes provided for in The 2026 Finance Act relating to the Management Package, please refer to our tax alert on this subject.

« BSCPE » Warrants for Business Creator Shares (Article 25)

The 2026 Finance Act increases the attractiveness of employee share option plans (BSPCE). Find out more in our dedicated tax alert.

The ‘Jeanbrun’ measure (Article 47), the new ‘private landlord’ regime

A new tax regime for ‘private landlords’, also known as the “Jeanbrun” tax scheme, has been introduced.

Applicable to unfurnished rentals, this tax regime is intended to make this type of renting out of property more attractive, in particular compared to furnished rentals.

It allows landlords, who are individuals, investing directly in a property or via a company not subject to corporation tax, to deduct from their property income a depreciation allowance of up to 80% of the property’s purchase price (after deducting the value of the land, estimated at a flat rate of 20% of the purchase price).

The annual depreciation rate is between 3.5% and 5.5%, depending on the nature of the tenancy and housing category (intermediate, social or very social) and the type of property (old or new).

Land losses including depreciation (but excluding loan interest) are deductible from total income up to an annual limit of €10,700, with any excess being deductible from property income over the last ten years. However, the total depreciation is capped at €8,000 per year. This amount is increased by €2,000 or €4,000 respectively in the case of social or very social housing.

This scheme is subject to strict conditions of eligibility. In particular, it provides for a cap on rents, a minimum nine-year rental commitment and, for older properties, the carrying out of works which constitute ‘major renovations’, representing at least 30% of the purchase price of the property. Renting such properties out to close family members is prohibited.

In the event of the property being sold, the capital gain is calculated based on the purchase price of the building or shares, less the amount of depreciation allowed as a deduction under the scheme.

The scheme applies to property purchases, as well as to applications for building permits submitted between 20 February 2026 and 31 December 2028.

New rules on the tax deductibility of payments into retirement savings plans (PER) (Articles 9 and 10)

Under the tax regime for PERs (retirement savings plans), payments made into such plans are deducted from taxable income when calculating income tax. This allowance is capped and any unused portion of the allowance may be carried forward to one of the following three years.

The Finance Act makes the following two amendments:

These measures apply from the 2026 tax year.

The 2026 Finance Act provides for two changes regarding tax relief for donations made:

Amendments to the regime for professional furnished rental property owners (LMP) for non-residents (Article 53)

The Finance Act stipulates that revenue from furnished rentals must now exceed the cumulative total of any taxable income from employment activity in France and any income received of a similar employment nature which is subject to an equivalent tax in the country of the taxpayer’s residence.

This measure applies from the 2026 tax year onwards.

For further details on the changes relating to furnished rentals, please see our dedicated tax alert.

PFU, the single flat-rate tax: elimination of the irreversibility of the progressive tax scale option (Article 126, I-3°)

Investment income and capital gains subject to the single flat-rate tax (PFU) may be taxed annually according to the progressive income tax scale, and this, on an optional basis.

This option, which previously was irrevocable, must be expressly opted for at the time of filing the tax return.

It is now possible to revoke the option retrospectively, within a specified time limit of amendment.

This measure applies from the 2026 tax year onwards.

More stringent requirements for the declaration of occupancy of residential premises (Article 126, I-6° and 14°)

Since 2023, owners of properties used for residential purposes must declare information regarding the occupancy of these properties to the tax authorities before 1 July each year.

From now on, rented property managers must also provide this required information relating to the occupancy of residential properties to those owners who request it.

Property managers include holders of a lease or agreement for the provision of premises that are sublet, as well as property management companies that have entered into a commercial lease and sublet any accommodation, this being the case notably in student or retirement homes.

The responsibility for updating this declaration may also be delegated to them. In this case, the penalty of €150 per property in the event of failure to declare, omission or inaccuracy is payable by the property manager.

As from the 2024 income tax return onwards, individuals who occupy second homes they do not own must provide details of these properties as well as details concerning the identity of the owners.

Failure to declare will now result in a 10% surtax on the housing tax. In the event of deliberate non-compliance, the rate may be increased to 40%.

These provisions apply from 20 February 2026.

Impartiate Tax Regime, determination applicable remuneration professional soccer player

The Finance Act 2025 was adopted by Parliament on 6 February 2025 and enacted on 14 February 2025.