Impatriation bonus and spreading of income received by sportsmen and sports women

Tax alertImpatriation bonus athletes

The Finance Act 2025 was adopted by Parliament on 6 February 2025 and enacted on 14 February 2025.

The legislation concerning individuals is more far-reaching than in previous years. The most significant measures concern the introduction of a minimum tax on high incomes and the regulations on the taxation of management and employee incentive schemes (or management packages).

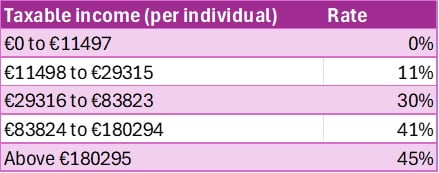

All the tax brackets will be raised by 1.8%:

The standard withholding tax rates will also be adjusted with effect from the 1st day of the 3rd month following the enactment of the law.

A tax differential on high incomes has been introduced for taxpayers resident in France for tax purposes and whose adjusted reference tax income exceeds €250,000 in the case of single, widowed, separated or divorced individuals, and €500,000 in the case of households subject to joint taxation.

The measure introduces an effective minimum tax rate of 20% for these taxpayers, based on their reference tax income less:

In the case of exceptional income (that which is not earned on an annual basis and which is in excess of the average net income for the last three years) one quarter of the amount is retained and added to the amount of total ordinary income for the calculation of tax payable.

The new contribution equals the difference between 20% of the income defined above and the amount of tax paid, i.e. income tax (increased by any tax benefits provided by tax reductions and up to the limit of the tax due, by certain tax credits), increased by withholding taxes paid after the date of publication of the law and by the Exceptional Contribution on High Income (CEHR) The amount is increased by €12,500 for taxpayers subject to joint taxation and by €1,500 for each dependent.

A smoothing mechanism is to be provided for in cases where income is between:

The contribution will apply to 2025 income only.

An initial instalment representing 95% of the contribution will be paid between 1 December 2025 and 15 December 2025.

In the event of non-payment or late payment of the initial instalment, or in the event of payment of less than 20% of the amount normally due, a 20% surcharge will be applied.

With effect on donations made the day following the enactment of the Finance Act:

Donations made between the day following the enactment of the Finance Act and 31 December 2026 that are used to purchase a newly built property or a property in the process of being completed, or to carry out certain energy-efficiency renovation work on the principal residence, may be exempt from transfer duties.

Sums of money donated must be done so in full ownership to a child, grandchild, great-grandchild or, where there is none, a nephew or niece.

The exemption is subject to:

The French tax administration's right to reclaim tax has been extended to the end of the tenth year (instead of the third year) following the year in respect of which the tax is due when an individual claims a false tax residency abroad.

This new deadline applies to an inspection of income tax, property wealth tax and transfer duty returns.

This new right may be applied to reassessment periods expiring on or after the day after the Finance Act is enacted.

With effect from the day following the enactment of the Finance Act, earnings from management packages are subject to capital gains tax, up to a ceiling equivalent to three times the company's financial performance during the holding period (see our specific alert on this subject).

Excess gains are taxed as salary and wages (on a progressive scale). The changes to this treatment will apply from the day following the enactment of the law.

A flat-rate employee contribution of 10% applies to the amount of net gains realised on securities subscribed or acquired by employees or directors, or allocated to them, in respect of the performance of their duties within the company issuing the securities or any company in which the latter directly or indirectly holds a share of the capital when these gains are subject to income tax as salaries and wages.

This employee contribution will apply to share disposals up to 31 December 2027.

The Finance Act amends the Social Security Code accordingly (Art. L 137-42).

A tighter legislation on the treatment of subscription warrants or rights and securities acquired on exercise of such warrants or rights (Article 92).

1. Subscription or allocation rights or warrants and securities received on exercise of these rights or warrants may no longer be placed in certain savings plans.

The Finance Act confirms the position of the administrative doctrine by prohibiting:

These new restrictions apply to the above-mentioned rights or warrants allocated or exercised on or after 10 October 2024.

In the case of rights or warrants which have been held in savings plans prior to 10 October 2024, the holder may withdraw them from the plan and make a compensatory cash payment within a maximum of two months from the date of withdrawal for an amount equal to the value of the rights or warrants at that date. This compensatory payment will not be taken into account in the set ceiling amount for authorised payments into the plan.

2. Distinction made between the gain on exercise and the gain on disposal of BSPCEs

The tax treatment of BSCPEs issued since 1 January 2018 made no distinction between the gain on exercise and the gain on disposal and only taxed the net gain arising from the difference between the disposal price of the securities and the issue price of the warrants. This net gain is now subject to income tax under a specific regime for BSPCEs (Article 163 bis G, I of the French General Tax Code).

The Finance Act now makes a clear distinction between two types of gain:

The two types of gain are subject to social security contributions as income from assets.

This amendment applies to all “securities subscribed” in the exercise of warrants as from 1st January 2025.

The tax regime for capital gains realised on the disposal of non-professional furnished rental property has been amended.

Presently, taxpayers do not have to add back the depreciation deducted from their rental income in the calculation of the taxable capital gain when the property is disposed of.

For tax purposes and in the calculation of the taxable gain, the initial purchase price of the property must now be reduced by any depreciation deducted during the rental period.

Depreciation relating to building works (construction, reconstruction, extensions or improvements) does not, however, have to be added back.

Certain types of property are exempt from this new rule, such as serviced residences for seniors and students.

This new measure applies to the sale of property from the day following the enactment of the Finance Act.

Article 150-0 D ter of the French General Tax Code provides for a fixed allowance of €500,000 on capital gains realised by executive managers of SMEs who dispose of their shares on retirement.

This tax credit was set to end on 31 December 2024 but has been extended until 31 December 2031 by the new Finance Act.

The regional councils in France may increase the rate of land registration tax or stamp duty on the sale of real estate to more than 4.50%, without this rate exceeding 5%. This provision would apply temporarily to deeds and agreements signed between 1 April 2025 and 31 March 2028.

This measure cannot be applied when the property purchased is a first-time property for the buyer and is intended for use as his or her principal residence.

Conversely, regional councils may also reduce the rate of or exonerate first-time buyers from land registration tax or stamp duty.

The reduction or exoneration is subject to the purchaser undertaking to use the property exclusively and continuously as their principal residence for a minimum period of five years from the date of acquisition.

The entry into force of these measures depends on the date of the decisions taken by the departmental councils.

Impatriation bonus athletes

3% Tax on French Real Estate Assets : any inaccuracy in the information provided on the form will result in the payment of the tax